LOM Comments 1

Add a comment

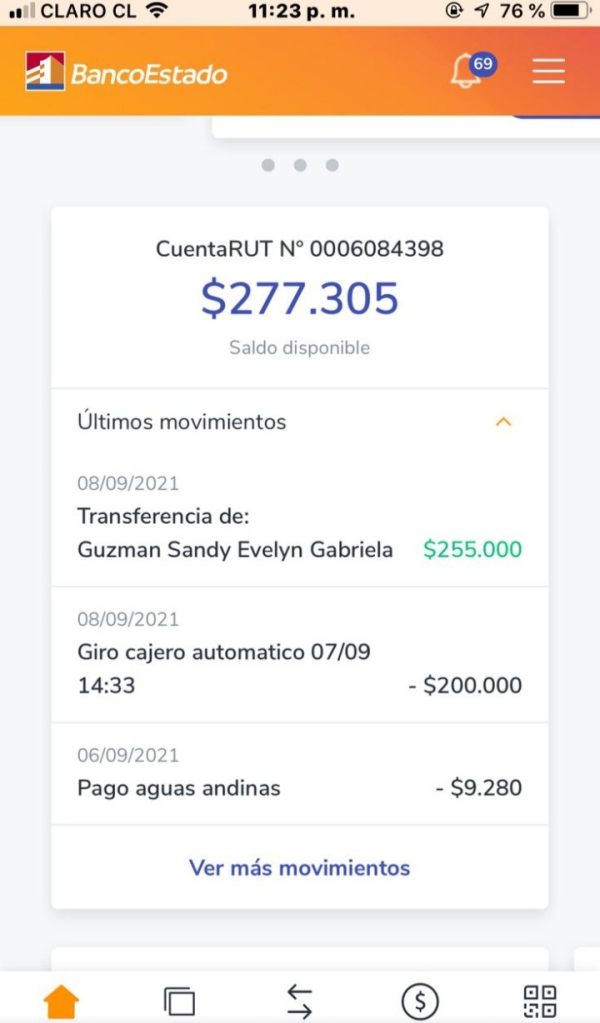

Exposure

It left quicklyMy money just as it came in, it was gone in one quick transaction and all gone, what a sad charge for that $277.

FX1407470498

2021-11-07

LOM Forex Broker provides real users with * positive reviews, * neutral reviews and 1 exposure review!

Access to various financial instruments, including forex, CFDs, commodities, and indices. Low initial deposit requirements, making it accessible for beginner traders. Good customer support and execution speed, as indicated by user ratings.

Access to various financial instruments, including forex, CFDs, commodities, and indices. Low initial deposit requirements, making it accessible for beginner traders. Good customer support and execution speed, as indicated by user ratings. Unregulated status raises concerns about safety and reliability for traders. Limited transparency regarding company ownership and operational practices. Negative reputation with numerous complaints about withdrawal issues and overall trustworthiness.

Unregulated status raises concerns about safety and reliability for traders. Limited transparency regarding company ownership and operational practices. Negative reputation with numerous complaints about withdrawal issues and overall trustworthiness.My money just as it came in, it was gone in one quick transaction and all gone, what a sad charge for that $277.

This lom review looks at a financial services company that has worked in the investment sector for over thirty years. LOM Financial Group started in 1992 and offers private investment services and products, including brokerage, custody, asset management, and corporate finance services. The company mainly targets wealthy individuals and institutional clients, which shows they focus on smart investors rather than regular retail traders.

LOM has stayed in the financial services industry for a long time. Specific details about their forex trading offerings, regulatory framework, and operational standards remain limited in public sources. The company's long history in the market shows some operational stability, though without full data on trading conditions, platform features, and client feedback, a complete assessment of their competitive position proves challenging.

The target customers appear to be wealthy individual investors and institutional groups seeking complete financial services beyond basic retail trading. However, potential clients should do thorough research given the limited transparency about specific service terms and regulatory oversight.

This review is based on limited available information and may not show the complete scope of LOM's current offerings or operational standards. Different regional groups within the LOM company may operate under different regulatory frameworks and service terms, which could greatly impact the client experience depending on location.

The assessment method relies mainly on publicly available information, and readers should note that complete details about trading conditions, regulatory compliance, and client service standards were not easily available during the research process. Prospective clients are strongly advised to request detailed information directly from LOM and verify regulatory status independently before making any investment decisions.

| Evaluation Criteria | Score | Rating Basis |

|---|---|---|

| Account Conditions | Not Rated | Specific account terms and conditions not disclosed in available sources |

| Tools and Resources | Not Rated | Trading tools and analytical resources not detailed in accessible information |

| Customer Service | Not Rated | Client support structure and service quality data unavailable |

| Trading Experience | Not Rated | Platform performance and execution quality information not provided |

| Trust Factor | Not Rated | Regulatory details and safety measures not comprehensively documented |

| User Experience | Not Rated | Client feedback and usability assessments not found in available sources |

LOM Financial Group started in 1992. The company established itself as a Bermuda-based financial services organization with a focus on private investment solutions. The company has built its business model around serving wealthy individuals and institutional clients, placing itself in the premium segment of the financial services market rather than competing in the mass retail trading space.

The organization's service portfolio includes brokerage services, custody solutions, asset management, and corporate finance advisory services. This varied approach suggests LOM operates as a complete financial services provider rather than specializing only in forex or CFD trading. The company's focus on private investment services shows a business model that values relationship-based client service over high-volume, low-touch retail trading operations.

According to available information, LOM has kept its headquarters in Bermuda while developing a global business presence. However, specific details about the company's regulatory oversight, trading platforms, asset classes offered for trading, and operational infrastructure remain unclear from publicly available sources. This lom review notes that the lack of detailed operational information may reflect the company's focus on private client services rather than public retail trading offerings.

Regulatory Oversight: Available sources do not specify the regulatory authorities overseeing LOM's operations or provide details about compliance frameworks governing their services.

Funding Methods: Information about deposit and withdrawal options, processing times, and associated fees has not been disclosed in accessible documentation.

Minimum Investment Requirements: Specific minimum deposit or investment thresholds for accessing LOM's services are not detailed in available sources.

Promotional Offerings: No information about bonus programs, promotional campaigns, or special offers has been identified in the research materials.

Tradeable Assets: The specific financial instruments available for trading through LOM's platforms have not been fully documented in accessible sources.

Cost Structure: Details about spreads, commissions, overnight financing charges, and other trading-related fees are not available in public documentation. This represents a significant information gap for this lom review.

Leverage Ratios: Maximum leverage offerings and margin requirements have not been specified in available materials.

Platform Options: Information about trading platforms, software solutions, and technological infrastructure has not been detailed in accessible sources.

Geographic Restrictions: Specific limitations on service availability by country or region have not been documented in available information.

Language Support: Customer service language options and multilingual support capabilities are not specified in accessible materials.

The evaluation of LOM's account conditions faces major limitations due to the absence of specific information about account types, structures, and requirements in publicly available sources. Traditional retail brokers typically offer multiple account tiers with different minimum deposits, features, and service levels, but LOM's focus on wealthy individuals and institutional clients suggests a different approach to account structuring.

Without access to detailed account documentation, it becomes impossible to assess the reasonableness of minimum investment requirements or compare LOM's offerings to industry standards. The account opening process, verification requirements, and onboarding procedures remain undocumented in available sources, making it difficult for potential clients to understand what to expect when engaging with the firm.

Special account features such as Islamic-compliant trading accounts, managed account options, or institutional-grade custody services may be available given LOM's positioning in the private wealth management space, but specific details are not accessible. This lom review cannot provide meaningful analysis of account conditions without more complete information about the firm's client onboarding and account management processes.

The lack of transparency about account structures may reflect LOM's business model of providing customized solutions to wealthy clients rather than standardized retail trading accounts.

Assessment of LOM's trading tools and analytical resources proves challenging due to the limited information available about their technological infrastructure and client support systems. Most established financial services providers offer complete research capabilities, market analysis, and trading tools, but specific details about LOM's offerings in these areas are not documented in accessible sources.

Educational resources, which have become standard offerings among retail-focused brokers, may not be a priority for LOM given their focus on smart institutional and wealthy individual clients who typically possess advanced market knowledge. However, even experienced investors benefit from quality research and analytical tools, making this information gap significant.

Automated trading support, algorithmic trading capabilities, and API access are increasingly important features in modern financial services, particularly for institutional clients. The absence of information about these technological capabilities makes it difficult to assess LOM's competitiveness in serving smart trading clients who may require advanced execution and connectivity solutions.

Third-party integrations, portfolio management tools, and risk management systems are often crucial components of institutional-grade service offerings, but details about LOM's capabilities in these areas remain undocumented in available sources.

Evaluating LOM's customer service capabilities requires information about support channels, response times, service quality standards, and client communication protocols, none of which are detailed in accessible sources. Wealthy individuals and institutional clients typically expect premium service levels, including dedicated relationship management and rapid issue resolution.

The availability of multiple communication channels such as phone support, email assistance, live chat, and in-person consultation services would be expected for a firm serving wealthy clients, but specific details about LOM's support infrastructure are not documented. Response time commitments and service level agreements, which are particularly important for time-sensitive trading and investment decisions, remain unspecified.

Multilingual support capabilities could be crucial for a firm with global operations, but information about language options and international client service standards is not available in the research materials. The absence of documented service standards makes it impossible to assess whether LOM meets the elevated expectations typically associated with private wealth management services.

Client relationship management approaches, dedicated account management, and personalized service offerings are often key differences in the wealthy client segment, but LOM's specific approach to client service remains undocumented in available sources.

The assessment of LOM's trading experience requires detailed information about platform stability, execution quality, order management systems, and overall trading infrastructure, none of which are fully documented in available sources. For institutional clients and smart individual traders, execution quality and platform reliability are fundamental requirements that can significantly impact trading outcomes.

Order execution speed, slippage rates, and fill quality are critical performance metrics for any trading platform, but specific data about LOM's execution capabilities is not available in accessible documentation. The absence of performance benchmarks makes it impossible to evaluate how LOM's trading infrastructure compares to industry standards or competitor offerings.

Mobile trading capabilities have become essential even for wealthy clients who may need to monitor positions and execute trades while traveling or away from their primary trading setups. However, information about LOM's mobile platform offerings and functionality is not detailed in available sources.

Trading environment stability, system uptime, and technical reliability are particularly crucial during volatile market conditions when clients need consistent access to their accounts and positions. This lom review cannot assess these critical operational aspects due to the lack of available performance data and client feedback regarding platform reliability.

Evaluating LOM's trustworthiness requires complete information about regulatory oversight, capital adequacy, client fund protection measures, and operational transparency, most of which are not detailed in publicly accessible sources. For a firm handling wealthy client assets, regulatory compliance and safety measures are paramount concerns.

The absence of specific regulatory information makes it impossible to verify LOM's compliance with applicable financial services regulations or assess the level of client protection provided by relevant regulatory frameworks. Different jurisdictions offer varying levels of investor protection, making regulatory clarity essential for potential clients.

Client fund segregation, deposit insurance coverage, and custodial arrangements are fundamental safety measures that smart investors expect from their financial services providers. However, specific details about LOM's asset protection measures are not documented in available sources.

Corporate transparency, including financial reporting, ownership structure, and operational governance, contributes significantly to institutional credibility. The limited publicly available information about LOM's corporate structure and operational transparency represents a significant consideration for potential clients conducting due diligence.

Assessing the overall user experience with LOM requires complete feedback from existing clients, detailed information about service delivery, and insights into the firm's approach to client satisfaction, none of which are readily available in accessible sources. Wealthy individuals and institutional clients typically have elevated expectations regarding service quality and user experience.

Interface design and platform usability are important factors even for smart clients who require efficient access to account information, trading capabilities, and portfolio management tools. However, specific details about LOM's user interface design and platform usability are not documented in available sources.

The onboarding process for new clients, including account opening procedures, verification requirements, and initial setup assistance, can significantly impact the overall client experience. Without detailed information about these processes, it becomes difficult to assess whether LOM provides the level of service sophistication expected by their target clientele.

Account management efficiency, including position monitoring, reporting capabilities, and portfolio analysis tools, are crucial components of the user experience for investment-focused clients. The absence of specific information about these capabilities limits the ability to evaluate LOM's user experience completely.

This lom review reveals significant information limitations that prevent complete evaluation of the firm's services and capabilities. While LOM Financial Group's establishment in 1992 and focus on wealthy individuals and institutional clients suggests a legitimate business operation, the lack of detailed information about trading conditions, regulatory oversight, and service standards creates substantial uncertainty for potential clients.

The company appears positioned to serve smart investors seeking complete financial services rather than retail traders looking for standard forex or CFD trading platforms. However, without access to specific details about account conditions, trading infrastructure, regulatory compliance, and client service standards, it becomes impossible to provide definitive recommendations about LOM's suitability for any particular investor profile.

Prospective clients, particularly those in the wealthy and institutional categories that LOM appears to target, should conduct thorough independent due diligence and request detailed information directly from the firm before making any commitment to their services.

FX Broker Capital Trading Markets Review